Anyway, enough with the excuses, It is exactly two years since my investing experiment began, so I thought I should give an update.

Changes to the portfolio:

First, just a quick word about changes to the portfolio:

30 October 2014: Sold Matchtech and bought Barratt

18 November 2014: Sold Renew and bought Bellway

10 December 2014: Sold Amec and bought Berkeley

The first thing to note is that there have not been any changes in the last five months. I am afraid that this is down to pure neglect on my part. Despite this, nothing in the current portfolio is below the sell limits. This may sound like an excuse, but I am coming to the view that a quarterly review strategy might work better than one that is constantly monitoring buy and sell signals.

An Overly Concentrated Portfoilo?

The second point to note is that these new purchases are all in the construction/property sector and so the portfolio has become rather concentrated (and it already held Persimmon). I don't have rules to manage sector diversity, so this is simply the way the cookie crumbled. I admit to being a little concerned about this, but not overly so.

When stocks across a sector are generating both high Stockranks and appearances across multiple screens, then I think it makes sense to view this as a high "StockRank Sector" and I am quite happy being overweight in it. This certainly seems to have paid off.

The construction/property stocks over the past 6-12 months have been the main engine of capital growth for the MB portfolio. Similarly, earlier in this experiment, the portfolio held a number of employment agencies which all played out well to varying degrees, with Staffline more that doubling in value.

The general consensus on Stockopedia seems to advocate sector weighting to ensure broad exposure to different types of stocks. I don't really see the point in this. What would have been the point of having equal sector weighting in energy stocks 6 months ago when the the sector was tanking? I would rather be invested in a sector that was cheap and building momentum... like construction.

However, I concede that four construction/property sector stocks in a portfolio of 15 is taking things a bit far and I should have a means of limiting this, to say, three. So one method would apply a strict limit. Another approach might be have a wider pool of possible stocks (e.g. all those with a StockRank greater than 90) and select a portfolio of stocks at random. This would tend to avoid the glut of construction/property stocks that keep popping up right at the top of my screen which currently looks like this (construction/property stocks highlighted):

This also happens to fit with one of my new ideas, which is to consider all 90-plus stocks, not just those with the very highest StockRanks.

Performance Overview

So how have things panned out over the past two years? The value of the Mechanical Bull portfolio has increased by 67.7 per cent since 24 May 2013 and so my initial £30,000 investment is now worth £50,313. The following chart shows that performance has completely trounced that of the main indices:

If one compares performance over the past year (18.6 per cent), this still looks very good against the FTSE 100 (3.2 per cent), but it was only slightly better than the FTSE 250 (15.9 per cent). Thus, the out-performance has very much been driven by the very good returns in the first year.

Where to now?

I feel this experiment has run its course and so this will probably be my last update on it. However I learned a lot from doing it:

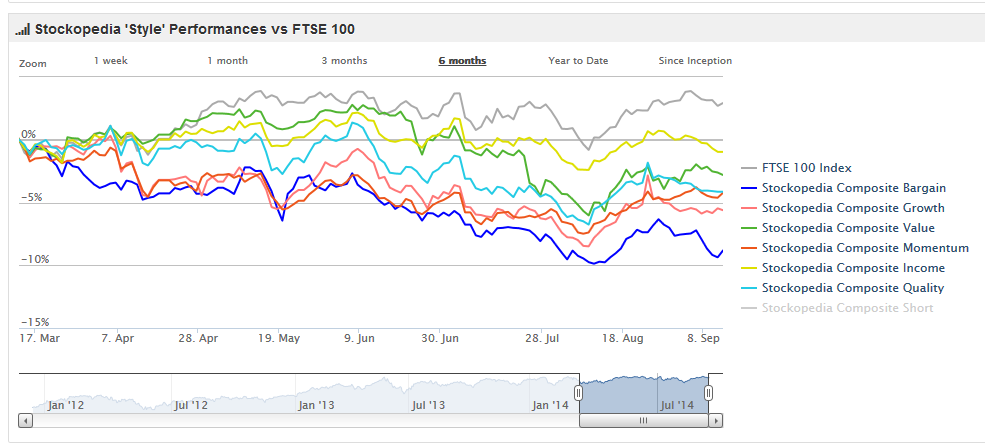

- Stockpedia's StockRanks perform well in aggregate over the long-term. These performance charts demonstrate this very clearly.

- Individual high StockRank picks do not work out every time. However, investing is a game of percentages and StockRanks offer very good odds.

- Even in aggregate, StockRanks do not work all the time. High StockRanks did not outperform the general market between about Feb 2014 and October 2014. Investing is a game of patience.

- There is no evidence that incorporating a "Screen of screen" metric helped improve returns. As the StockRank performance charts show I could have expected very similar returns from a random set of 90-plus StockRank stocks.

- Monthly checks against the buy and sell rules may be too frequent and may have resulted in bailing out of winning picks too soon. Again, investing is a game of patience. A quarterly based review with rebalancing within set limits would probably have been more effective.

- Fifteen stocks does not offer enough diversification against picks that go pear-shaped. I agree that 25 to 30 is sensible for the average private investors.

- Mechanical investing works! My real life portfolio has achieved similar returns over the past two years and dreams of financial independence suddenly seem much closer.

Idea 1: High StockRank with low PEG

As I've said, I am not convinced that the Screen of Screens as a particularly useful metric. It has returned 35 per cent over the past 2 years, which is some way short of what one could have achieved from a simple 90-plus StockRank based system.

But then how should one select from the pool of high StockRanks to get improved performance?

A metric that looks interesting the PEG ratio, popularised by Jim Slater. A backtest of the Sharelock Holmes StockRank equivalent of top 8 per cent ranked stocks gives a 16.5 per cent average annual return over the past 10 years. However, if you throw in a screening rule of PEG less than 1, the annualised return increases to over 27 per cent. I'm now using this screen on Stockopedia as the foundation of my stock picks.

Idea 2: CAPE Asset Allocation Strategy

A recent post on the Stockopedia discussion board mused on where the next market crash would come from. I don't have any answers but I am very interested in how best to protect my capital whenever it happens. From what I can tell StockRanks are unlikely to provide much protection and so one really need to be thinking about asset allocation.

This article from John Kingham (UK Value investor) is over 5 years old, but it is the single most influential thing I have read over the past 12 months. The basic concept is to use the FTSE 100 Cyclically Adjusted Price Earnings (CAPE) as the basis for allocating capital between stocks and cash. When the CAPE is very low, one might go all in into stocks and when it is very high, one might move mostly into cash. The article demonstrates how over the long-term one can achieve similar returns to an "all in" strategy but with much lower drawdown (i.e. less risk).

This is essentially another mechanical based strategy based on historical evidence so it very much chimes with my investment philosophy. Based on Kingham's analysis, the FTSE 100 can be currently considered "slightly cheap".

I have started researching an asset allocation system but it is not yet ready for unveiling. No doubt a topic for a future blog post.

{kind=link}